Why should they invest in bonds and unit trusts rather than constructing their family home @33 Years.

We leave too much money on the table because of sleep.

This question arose yesterday during one of my investment and financial consultations. I had the pleasure of engaging in a particularly enlightening conversation with a couple considering their next step.

To provide context for this discussion and to ensure a smooth flow of information, I will share some details. The husband, a 33-year-old professional, and his wife, a 33-year-old medical doctor, are parents to two children. They are at a stage where they are beginning to plan and strategize their finances in the most effective manner, recognizing that they are no longer young and that every decision they make must be financially prudent—a commendable mindset that many of us would do well to emulate.

Their combined income, as they are both employed, is approximately 8 million Ugandan shillings net, which places them in a favorable income bracket in Uganda for a couple.

The initial question they posed was about their projected incomes over the next 5 to 10 years. The husband assessed that, given the nature of his work and his current income, he feels he has reached his peak. He does not anticipate a significant increase in income if he remains in the same line of work.

On the other hand, the wife believes she can potentially double her income in the next 10 to 15 years, as she is employed by the government.

Their salaries have reached a level that necessitates aggressive investment, as there is not much room for growth in terms of salary increments over the next 5 to 10 years and they at that age when we feel old, yet we still have over 20 years to go of working and building the Human resource capital.

This brings us to the crux of the conversation: should they construct a family home over the next three years, or should they invest their money? This is a simple yet profound question that many of us fail to ask ourselves.

At 33 years of age, should one build a family home or invest? The investment options are numerous, but my bias, as will become evident in our discussion, leans towards treasury bonds and Unit trusts.

At 33, they are millennials, still young, with many earning years ahead—assuming retirement at 60. With two young children, they are at an age where they can comfortably live in a rental property, as opposed to the significant emotional satisfaction that comes with owning a home. We must differentiate between financial and emotional perspectives.

Courtesy photo.

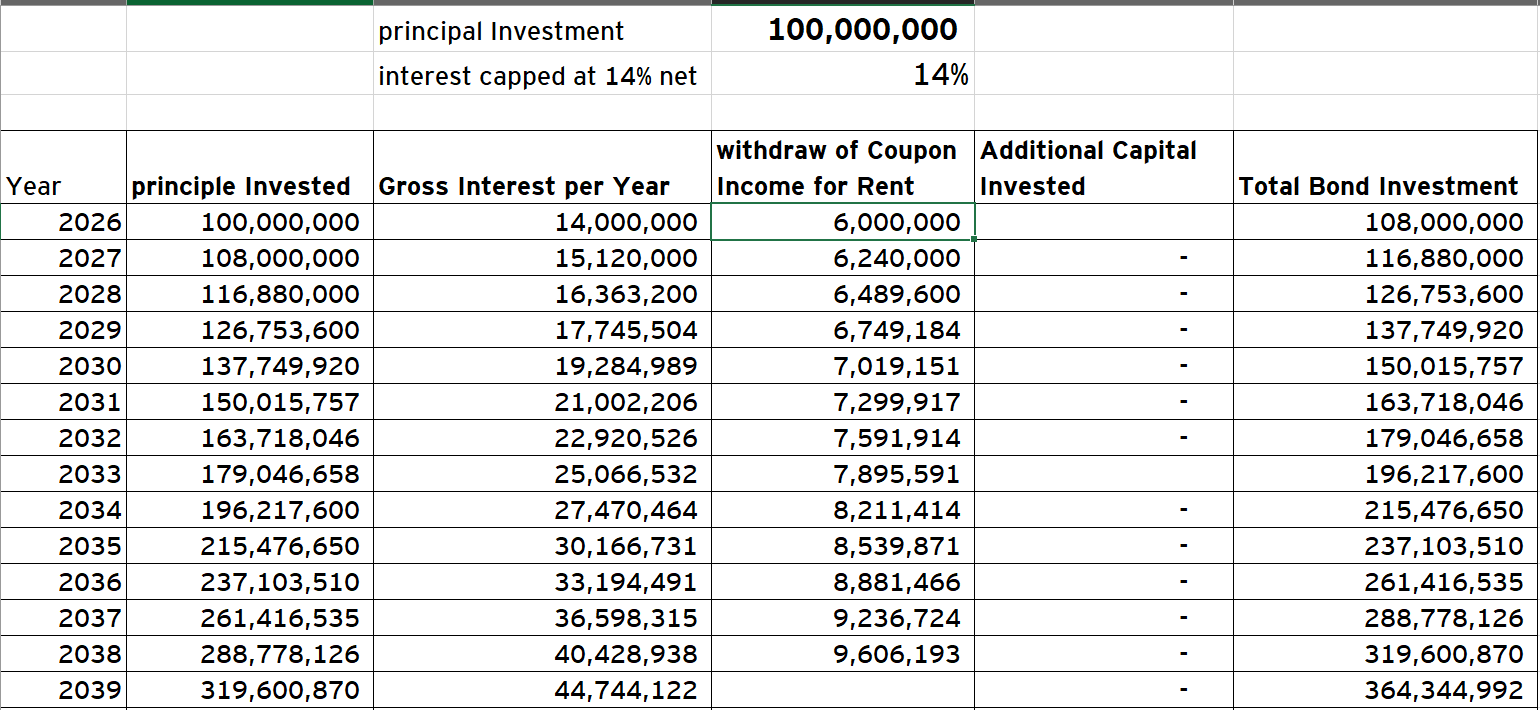

We examined the numbers. Constructing their family home would cost them a minimum of 100 million Ugandan shillings over the next three years, which equates to over 30 million shillings invested in a construction project annually.

By 2028, they would be able to move from renting to their own home. Another factor to consider is their current rental expenses, which average 500,000 Ugandan shillings per month. This amounts to an annual rental expense of 6 million shillings. If rent remains constant, which is unlikely as rental rates tend to increase, it would take them approximately 13 years to spend 100 million shillings on rent.

Factoring in a 5% rental cost increase per year, it would take them 13 years to incur 100 Million and that would take them 2037.

So, why construct a home in the next four years? The question becomes more intriguing when considering the potential of their investments. Where will they be in 13 years, at age 45, if they choose to invest rather than build? Will they be better off if they continue to rent and invest their money?

We introduced the option of investing in treasury bonds. At 33, their lives are still ahead of them, and the house they can afford now will likely still be within reach in 10 years. Seven years ago, in 2018, the cost of construction has not increased significantly. If they invest 100 million shillings in a house, they will not earn any income from it, except for the savings on rental expenses.

However, if they invest that UGX 100 million in a treasury bond with a 10-14% annual return, they could generate approximately 14 million shillings per year. This is more than enough to cover their annual rent of 6 million shillings, leaving a surplus of 8 million shillings to reinvest in treasury bonds.

Even if they are to invest that UGX 100 million in a bond and are to use some of the coupon income to pay rent, as shown below, by 2037 when they are 45 years, they would have over UGX 300 Million NetWorth in bonds. Then why would then then construct?

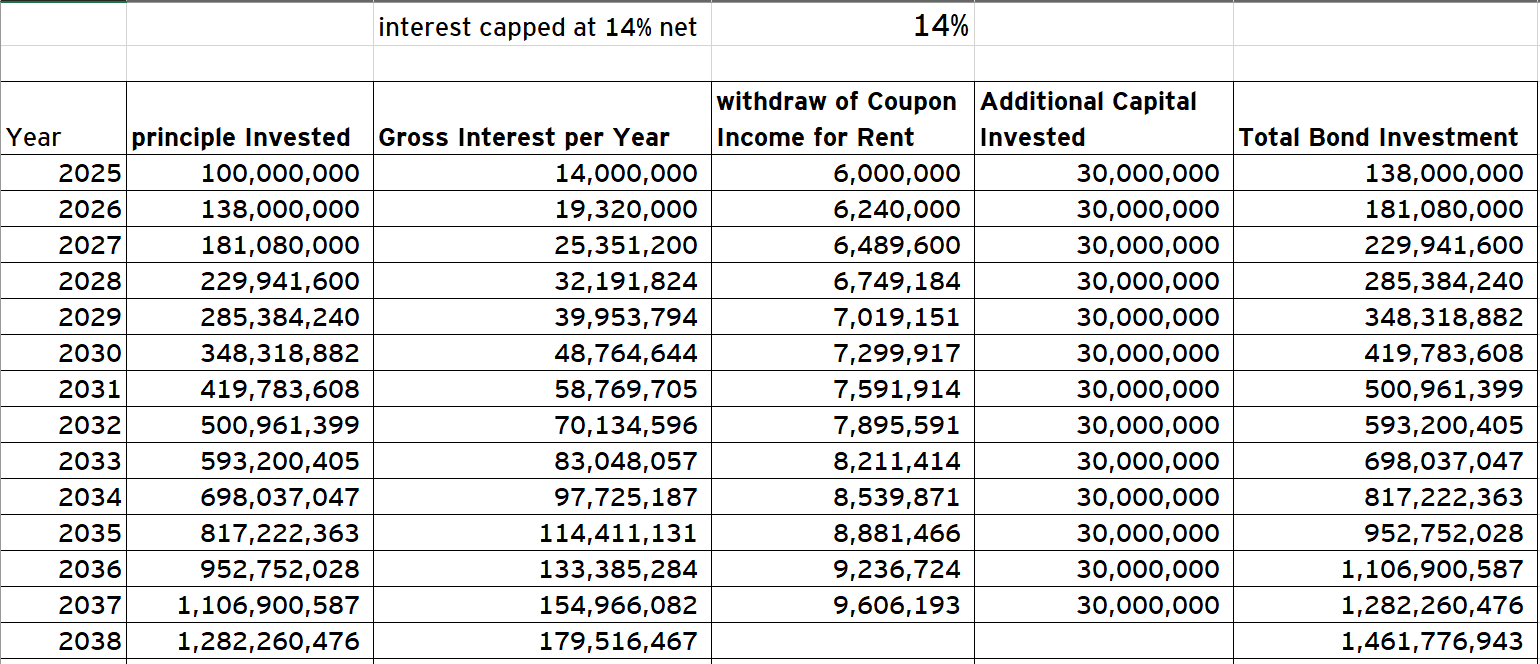

Currently, their monthly income as a couple is 8 million shillings, totaling 96 million shillings annually. If they incrementally add 30 million shillings annually as a family, which is about 1.5 million shillings per person per month, their asset base as a family could reach around 1.5 billion shillings by the time they are 45 and their children are in secondary school. Treasury bonds compound quickly; every five years, their money could potentially double. If they adhere to this plan, they could become billionaires in the Ugandan economy by age 45, earning over 100 million shillings in profits annually. At that point, they could construct a home or purchase any house they desire by liquidating just 10% of their portfolio.

One societal lesson we must learn is to let our money work for us before we spend it. Constructing a family home is a significant step, but it does not generate income; it only saves on rental expenses. Before committing to such a substantial investment, one should consider how much they would spend on renting a comparable house, which is often less than 10% of the house's value. If one can afford to construct a UGX 500 million house, why not invest that money in a way that generates more income, easily covering rental expenses plus more profits?

We need to move away from emotional investments, such as those made by our forefathers, who often left behind only a family home and a few plots of land, with no income. At the peak of their earning years, they focused on constructing a house, leaving money on the table. A family home is not a poor investment, but it should be made at the right time, using profits from investments rather than primary income. Liabilities like a family home should be funded by the profits of profits.

If you are concerned about the stability of renting, consider constructing rental properties instead. Rent out most units and live in one, allowing the rentals to generate income. Diversify your income to the point where it makes sense to spend on non-income-generating assets.

Courtesy photo.

Many people may have already constructed their homes without this knowledge, but now we understand the importance of investing our money to generate more income before considering upgrades or new constructions. Remember, a house depreciates over time, while 100 million shillings invested in a treasury bond can grow significantly, potentially doubling every five years.

We must think critically about our financial planning as a family. Young couples with some savings should prioritize investment over immediate home construction. By investing wisely, they can achieve a higher net worth in 10 years than if they had simply built a house. It's about allowing your money to compound quickly, starting with a substantial initial investment.

Happy Investing Everyone

Alex Kakande

the mathematics looks good, but practice usually is a whole other thing. starting off, not everyone has the 100m saved up to construct, especially salary earners. Many save as they build, and because of the construction, they tend to save more than they would otherwise to ensure progress. for a family of 4+1, earning 8m ( hopefully net), chances are their lifestyle is eating into 70% of that income, leaving them with at most 30 million a year, and that is if there do not have any other external expense for example school fees for a masters degree, parents, siblings and the non ending required support in our circles today. let us say they are brave enough to save the 30m, it will take them the next 3.5 years to save it. in the meantime their salaries are growing by almost 10% every two years, which is common for most job roles. 10% of 8m is 800k. the rent in Kampala is seemingly increasing at the rate of about 3 to 5% and if you add on family expansion, it can mean higher. and guess what, i have seen many couples where one of the incomes is lost, especially as they go into their 40s, which changes the mathematics totally.. do i think investing is wise? of course. However, life is not mere arithmetics, it is real. it is always important to take care of the basics first. 1. put food on the table, clothing on their backs, health care, and a roof over their heads. cover housing early, before kids fees sky rockets. dont aim for an expensive home, build a modest one that wont eat into your income. avoid going into your 40s when basic needs are still a challenge, it will mess up your ability to heavily invest.

i have read a lot of articles, and watched many videos that are trying to convince everyone that building wealth is a sprint, no my dear, it is a marathon. it is way easier to grow your wealth when the basics are out of your way.

once you have the basic needs fully covered, increase on your investment for retirement, and the children's education. and once these are taken care of, become even more generous now.

again, wealth building is not a mere mathematical equation, it is not a sprint, it is something you do diligently over time.

Hey Kakande, these numbers are always colorful, and inspirational, and God knows, I love you for that! I mean, you can make me want to sell all I have for Bonds and just sit back and not work anymore, waiting to become a billionaire in 10yrs and then buy back the world! But sometimes, they are too colorful! Why is a doctor and a professional renting a 500k house? Do you know what a 500k house looks like in Kisaasi, Kyanja, Kiwatule, Lungujja and Mengo? For a family of 4, and not counting the maid. Are they done having kids? It means soon they are renting a house at probably 1m for a 2 bedrooms with more decent amenities like compound, near schools and the like. Then school fees and the lot kick in because of the kids. Are they still able at that point able to add 30m annually to the bond? Yes they are young professionals, but not guaranteed to be employed pakalast, in this economy. Doctors too leaving government, and many are running around looking for gigs, and demanding private clinics for 6 months arrears. Maybe we should also look at plans where they can construct, and still save to build a decent bonds portfolio. I doubt that homes/houses are primarily built for sleep. But who knows! Thanks for the articles!