The Treasury Bond Boom: Why Banks Are Lending to the Government More Than to Customers

Stanbic Bank Review.

Friends,

In the recent Months, there is a growing concern that Banks are continuing to skew towards lending to Government of Uganda through buying treasury Bonds and bills than lending to Private sector and this is continuing to crowd out the Private sector in accessing friendly loans.

It’s an open secret that the high interest rates in Uganda are mostly also attributed to the high yields banks are getting from lending to government in the medium to long term bonds which is a risk-free investment for the banks thus pricing up the risk of lending to the private sector which is leading to extremely expensive interest rates in the country.

In this letter, we look at some local banks' investments in Treasury bonds. Why are they going so aggressive on Treasury bonds? Maybe this might inspire you to also to start diversifying and investing in Treasury bonds and also appreciate that they are not a too much a risky investment if Banks are going so aggressive on them.

Stanbic Bank Uganda.

The biggest bank in Uganda, has seen its investments in Treasuries move from a low of 777 billion Ugandan shillings to the current 3 trillion Ugandan shillings in the last 10 years. From 2014 to 2023, the growth rate of investments in securities outstripped that of growth in loans advanced to customers. In that same period, loans grew by 160% while investments in securities grew by over 300%.

This implies that the bank has consistently channeled more money at a higher rate to buying Treasury bonds than to lending to customers.

What are they seeing that we are not seeing?

Since 2020(Covid Period), the bank's loans to customers increased by only 17% (net of 622 billion Uganda Shilling increase), yet investment in government securities increased by 56% (1.14 Trillion Uganda shilling increase).

Loans Growth.

Stanbic Bank as the biggest Bank in Uganda by all Metrics, It has taken it 7 years to double the total loans advanced from a 2.17 Trillion UGX in 2017 to the 4.3 Trillion UGX in 2023 at a time when the economy was growing exponentially (Covid years not withstanding), which begs a question, why isn’t Stanbic Bank not doing enough to ensure a continued and consistent deepening of accessing to financing by the private sector especially at friendly levels? At Least Stanbic Bank can’t say the Losses on loans are that significant to them.

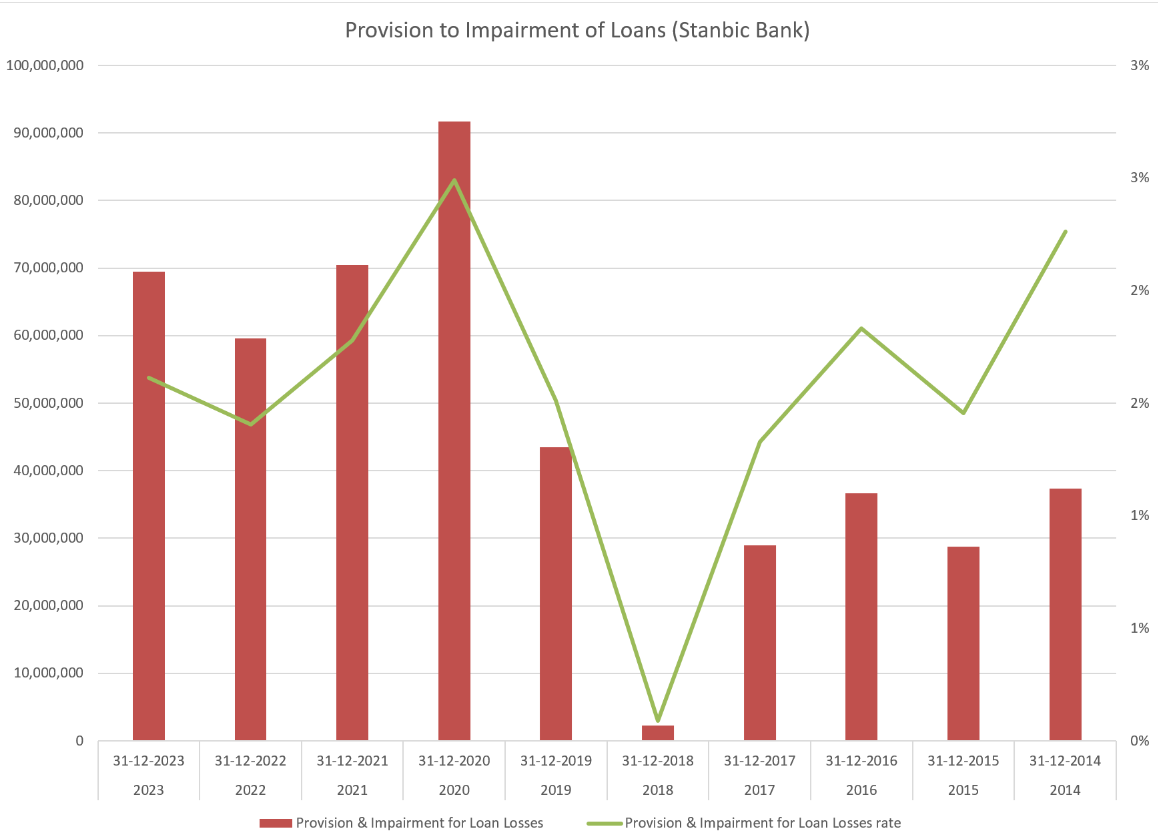

Stanbic Bank, like many other Banks is have a very low Impairment provision of around 2% with only the 2020 Covid year that led to a surge in Impairment loss provisions on loans of around 3% or 80 Billion UGX but a rate the bank has seen coming down to the average 2%, why is this then not reflected in the cost of lending to the Private sector with interest rates on lending dropped to lower levels of 14%-15% averagely as compared to the 17%-18% the private sector businesses are experiencing lately?

Whereas the Loans to Customers which is the critical ingredient of the growth of our economy is growing at a straight-line basis, the Investments in Bonds is growing at an exponential rate over the last 10 years and doubling every 5 years.

This level of Pivot, is profitable for the shareholders and the bank as seen in the Net Income earned by the Bank per Employee currently averaging 212 Million UGX per employee from the lows of UGX 71 Million in 2014, but what is the cost of it to the economy if the private sector isn’t accessing the critical financing at good rates?

This trend is almost the same for all banks in Uganda throughout. There is a consistent trajectory by banks to lend to the government through buying Treasury bonds and bills than to lending to customers.

Yes, loans to customers are still high compared to investment in Treasuries. But if the rates seen in the last 5-8 years were to continue, it won't be long before banks have investment in government securities as their biggest asset item on their Balance Sheet.

If you enjoyed this letter, please consider sharing it with your friends and families,

I hope you have a great week and potentially invest in Uganda’s Capital Markets.

Alex Kakande

The reasons the banks are turning to government bond could be manifold. First, shareholders returns from the high yields. Second, many of Uganda's private sector can hardly absorb as loans all the funds that the banks have. More so the private sector is very nascent, largely family owned with weak business models, poor management practices and low lifespan.

My key worry is why unlike in the past, BoU now want citizens to buy these bonds through the banks who will cream off at least 2.5% management fees? This secondary market transaction is both a sign of syndicated bond trade and rip off to local investors in the bond market.

And as you noted, it's time the CMA intensify Investment education (as you do here) to the increasing middle class Ugandans so that overtime we can crowd-in more citizens on the bond market (citizens lending to their own government and enjoying both the services and financial returns).