Rethinking Financing: Why Uganda Should Embrace Infrastructure Bonds

Feb 24, 205

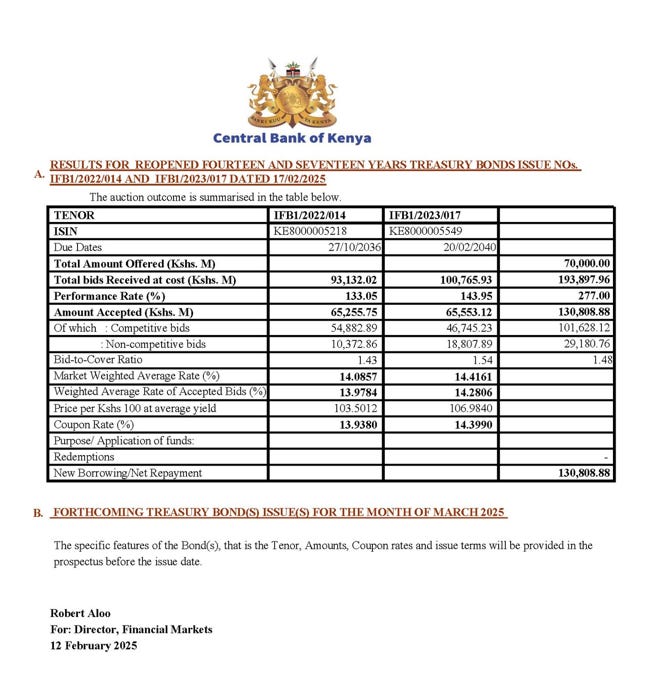

Last week, the Kenyan central bank auctioned off two infrastructure bonds that were highly subscribed, raising over 1 billion U.S. dollars from these bonds alone. Both bonds are long-term: one is for 14 years, while the other is for 20 years.

The Kenya’s Infrastructure Bond yield over a 2 year period.

The Kenyan community, particularly retail investors, contributed nearly 220 million U.S. dollars, while institutional investors invested over 780 million U.S. dollars. This indicates a growing demand in the country.

In Kenya, the infrastructure bonds attract a 0% withholding tax, meaning the coupon rate received is gross, with no tax payable. This has made them one of the most attractive investment vehicles for individuals looking to invest in capital markets. It continues to be observed that each time the government raises money through the issuance of an infrastructure bond, they are oversubscribed with good margins and yields, creating a win-win situation for the government, the economy, and the people.

Many other countries globally have issued infrastructure bonds, and one of their most appealing features is the 0% withholding tax. We have seen Kenya issue these bonds, along with a few other countries in Africa. This brings me to the case of Uganda. In Uganda, we only have treasury bonds denominated in Ugandan shillings; we do not have infrastructure bonds, euro bonds, or sukuk bonds, which are Islamic-compliant. Thus, the only type of bonds available in Uganda are standard Ugandan shilling treasury bonds.

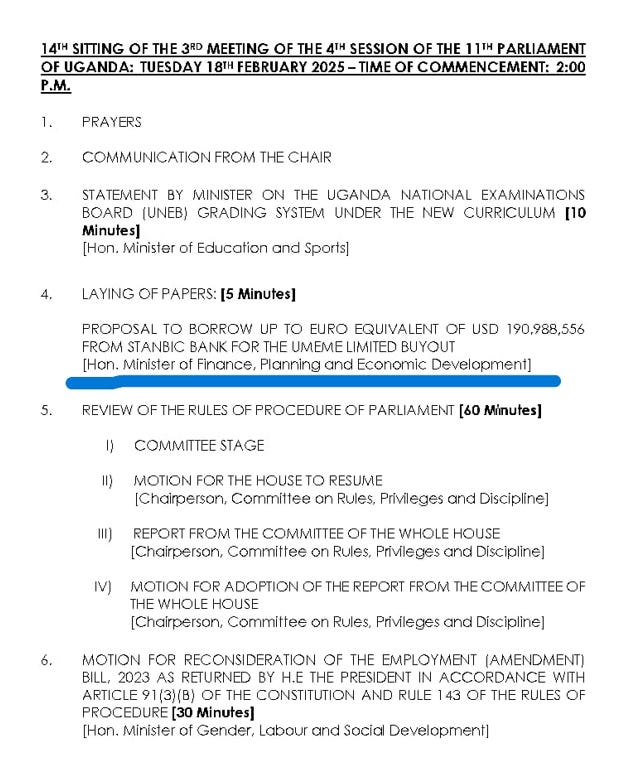

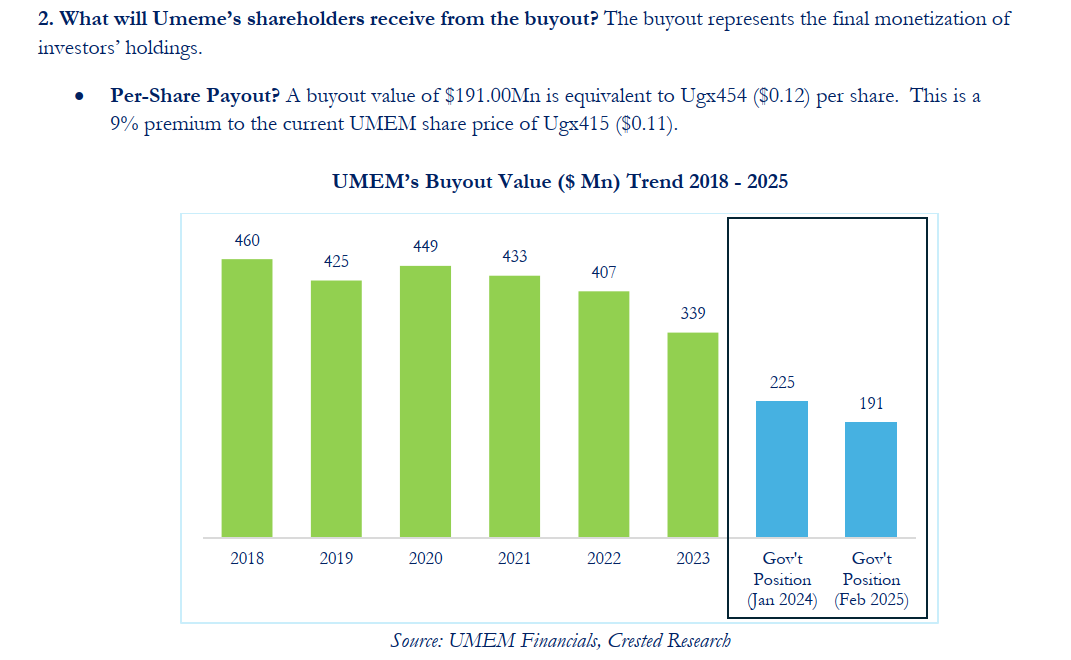

This week, we learned that the government has requested approval from Parliament to borrow a significant amount of money from Stanbic Bank Uganda to pay off UMEME concession due at the end of March. This has raised concerns among investors, particularly those UMEME shareholders, who own shares in the company, questioning whether the government has the capacity to pay them.

The government does have the capacity, depending on the avenues they choose. The question arises: why is the government opting for private commercial bank borrowing instead of exploring other available options to pay off this concession for electricity distribution, which should revert back to the government?

Infrastructure and electricity distribution fall under the infrastructure framework, which is why they are managed by the Ministry of Works.

Why hasn't the government considered issuing an infrastructure bond with the incentive of a non-withholding tax on the income generated from such an investment, even if it is a long-term bond?

This could help build confidence and attract more investors. The government needs to think outside the box to determine how to attract more individuals with liquid cash looking to invest. If other countries are doing it, why isn't Uganda exploring this option to fund its infrastructure?

Unless there are underlying issues within our country and its operators, why would the government choose to pursue expensive private credit to fund a fundamental infrastructure project when it could easily issue an infrastructure bond? There is a framework for infrastructure bonds, and we have seen them work; for instance, Kenya raised over a billion U.S. dollars. The government only needs around 200 million U.S. dollars for this payment concession payout.

They just need to raise approximately 200 million U.S. dollars. Why opt for a costly commercial loan instead of a longer-term infrastructure bond that would allow Ugandans to invest and explore capital market products?

Currently, the most expensive loans on the government's books are those obtained from private commercial banks, which are more costly than long-term treasury bonds.

Why wouldn't the government consider raising capital through treasury bonds to pay off the concession? If they are going to borrow from one private bank, they could have borrowed from the public at a better rate or structured the bond as an infrastructure bond with tax incentives. This would expand the range of bond offerings in the country, which is all we are asking for.

The government and the Ministry of Finance, currently facing scrutiny over embezzled funds that led to the interdiction of the Accountant General, and Director Debt Management Services are seeking the easiest way possible to address these issues. However, they also have a mandate to continue growing the capital markets and expanding the investment horizon of the economy.

It would be more effective and beneficial to raise funds for long-term infrastructure projects without straining the country's finances by utilizing public markets and issuing products like infrastructure bonds. If commercial banks wish to take advantage of these opportunities, they can still invest in them, just as they do with treasury bonds and other government offerings.

Happy Investing Everyone

Well said Mr.Kakande