The Price of Compliance: How Digital Tax Stamps Are Hurting Uganda's Manufacturers and Consumers

November 1, 2024

Friends,

The introduction of Digital Tax Stamps (DTS) in Uganda was heralded as a groundbreaking move to enhance tax administration, combat counterfeit goods, and provide real-time data for tax policy and administration. Launched by the Uganda Revenue Authority (URA) on November 1, 2019, the DTS system mandates all manufacturers and importers of designated products to affix digitally traceable tax stamps.

While the initiative aimed to protect government revenues and ensure fair market competition, it has also brought significant challenges, particularly for the manufacturing sector.

The Cost Burden on Manufacturers

For many manufacturers, especially Small and Medium Enterprises, the implementation of DTS has led to a substantial increase in operational costs. These costs include the procurement of hardware, software, and infrastructure required for DTS compliance.

Uganda Breweries Limited (UBL), for instance, has spent UGX 451 million on stamp applicator machines and over UGX 77 billion on stamps to date. This translates to an average annual expenditure of UGX 20 billion on stamps alone, not to mention UGX 840 million on incidentals. Despite reviews on the cost of stamps, the expense remains substantial.

But is this extra cost truly worth it to the business community or just increasing their operational expense with no net gain to the coffers of Uganda?

“Imagine the plight of a small and medium businesses who have to choose between investing in essential equipment and services to grow their business or complying with the costly DTS and other aggressive URA regulations. The financial strain is immense and currently hindering business growth. These businesses, which are the backbone of Uganda's economy, are being pushed to the brink. “

A study conducted by the Private Sector Foundation Uganda in collaboration with PwC confirmed these findings of a net cost of the implementation of the DTS System. The report highlighted that DTS has significantly impacted economic performance and job creation. Before DTS implementation, Local Excise Duty collections grew by 12%, reaching UGX 2.13 trillion from July 2016 to June 2019.

Post-DTS, there was a 7% decline in Local Excise Duty collections during the 2020 fiscal year, followed by a 13% increase from July 2020 to June 2023, totaling UGX 2.74 trillion. Overall, Local Excise Duty revenue grew by 9% from July 2016 to June 2023.

(The Entities have spent UGX 718 Billions just to increase the Local Excise duty by just UGX 612 Billion. That’s a Net cost of a policy rather a net benefit, which continues to beg a question, was it worth it?).

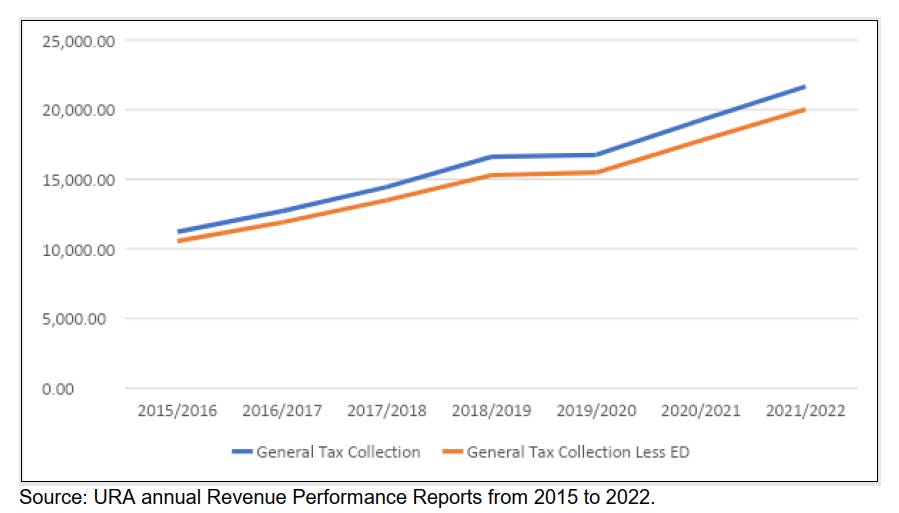

Has DTS really been the driving force behind the increase Tax collection by URA?

“for scenarios inclusive and exclusive of Local Excise Duty, there was no growth in tax collections from 2018/19 to 2019/20, followed by a subsequent recovery. Notably, the gap between general tax collection and tax collection excluding Local Excise Duty started widening in 2019 and continues to do so as the economy rebounds from the COVID-19 pandemic. This widening gap signifies an increasing contribution of Local Excise Duty to the overall tax collection. However, further analysis below illustrates that this gap ought to have widened more significantly if it had not been for the pandemic and introduction of DTS”.

Illicit Trade and Compliance Issues

Despite the DTS system's intentions, there has been no notable reduction in illicit trade. URA reported a loss of over UGX 91 billion in 2022 due to illicit trade. A 2021 Euromonitor study revealed that Uganda loses approximately USD 458 million (UGX 1.724 trillion) annually in unpaid taxes. The WHO’s Global Health Observatory database further confirms this, showing that the unrecorded amount of alcohol consumed per adult continues to grow exponentially, from 1.8 liters in 2018 to 5.6 liters in 2024.

The rapid implementation of the Digital Tax Stamps, though was aimed at increasing tax revenue and curbing illicit trade, has had a significant counter-effects. Businesses, especially SMEs, that are facing increased operational costs may create opportunities for corruption behavior, as officials demand bribes to facilitate compliance, and bureaucratic complexities further hinder business operations.

The Big question. The Consumer Impact

For consumers, the cost of goods and services often rises as businesses pass on their compliance costs (Businesses tend to pass on the cost of doing business to the final consumer).

In rural areas, especially constituting the Majority for Uganda, limited infrastructure and technology access may restrict the availability of products, impacting consumer choice.

Proposals for a Balanced Approach

To optimize DTS benefits and mitigate its adverse effects, several proposals have been put forward. These include:

DTS Cost Reductions: Reviewing and renegotiating current DTS agreements to address elevated fees and costs would reduce the financial burden on manufacturers.

Offsetting the Cost of Stamps Against Other Tax Liabilities: Adjusting excise duty rates to reflect the costs of implementing DTS would align both parties' interests and enhance the tax system's effectiveness.

Zero Rating the Cost of DTS Stamps for VAT Purposes: Exempting stamps from VAT would reduce costs for businesses, encouraging compliance.

Full Automation of the DTS Application Process: Automating the processes would enhance efficiency, minimize human errors, and reduce revenue leakage.

Cost-Free/Discounts on DTS: Providing cost-free DTS or offering discounts would significantly lower the financial burden on manufacturers and improve compliance.

Improved Responses to Complaints: Enhancing the response to complaints and introducing stricter penalties for offenders would support the broader goal of reducing illicit trade.

In the long term, introducing legislation for process losses, intensifying enforcement against illicit trade, and considering phasing out DTS for products with no evidence of under-declaration, counterfeit, or smuggling issues are crucial steps.

By addressing these challenges and implementing the proposed solutions, the government can create a more balanced and sustainable approach to tax administration that supports both manufacturers and consumers.

Alex Kakande

Unfortunately DTS was only subjected to cost-efficiency analysis without an extended analysis of its cost-benefit and cost-effectiveness. This is also akin to almost all our Ugandan taxes. Take a keen look at PAYE and you will note how payers are hurt by this frontloaded tax.

Its about time that our economists and legal fraternity joins to dive deeper into policy analysis and public interest litigations to bring checks and balances and sanity to the cabinet (blind poilcy originators) and MPs (blind policy endorsers). Unchecked, taxes will bury (because it has already killed - pun intended) this economy (e.g., the many micro and small enterprisers will be justifiably disincentivised to transition into formal firms).